1 No-Brainer Artificial Intelligence (AI) Stock to Buy With $370 and Hold for 10 Years

Earlier this year, Palo Alto Networks (NASDAQ: PANW) reported seeing a tenfold increase in the frequency of email-based phishing attacks compared to the same period in 2023. The jump is related to malicious actors using generative artificial intelligence (AI) to rapidly craft realistic content to trick employees into handing over sensitive information.

This change in tactics means businesses need to change the way they think about cybersecurity. Palo Alto is weaving AI into many of its products to make them faster and more automated, which can help combat AI-based threats. However, some businesses are also putting their valuable data at risk by experimenting with AI themselves in an insecure manner, so Palo Alto is releasing new tools to protect them, too.

Here's why investors with some idle cash -- money they don't need for immediate expenses -- might want to consider allocating $370 to Palo Alto stock and holding it for the next decade.

A leader in AI-based cybersecurity

Palo Alto's cybersecurity software portfolio is spread across three different platforms: cloud security, network security, and security operations. And the company is weaving AI into as many products within each category as possible.

The Cortex XSIAM security operations solution is a great example. Palo Alto says 90% of security operations centers within organizations still rely on manual processes, and human managers simply can't keep up with the sheer volume of alerts, so 23% of incidents are left uninvestigated. XSIAM uses AI to automate incident response and remediation, and Palo Alto says more than 50% of customers have reduced their median time to resolution (MTTR) to under 10 minutes -- from several days previously.

During fiscal 2024 (ended July 31), the number of customers using XSIAM soared fourfold compared to fiscal 2023, and bookings more than doubled to $500 million. Those are solid results considering the tool is only around two years old, and it highlights the surging demand for AI-powered security.

But as already mentioned, Palo Alto is also focused on protecting customers who are using AI. It's introducing new tools for its network security platform like AI Access Security, which assigns a risk score to hundreds of third-party generative AI applications. AI Access shows managers how employees are using those apps to ensure safe deployment, and the tool also offers data controls and an ability to block specific apps entirely.

Deployment couldn't be easier. All 5,000 existing Prisma Access customers will soon be able to use AI Access, and it will be as simple as flipping a switch. Around 1,000 customers expressed interest during the pilot program, so Palo Alto will soon unlock even more revenue from its existing users.

Image source: Getty Images.

The shift to platformization

Palo Alto generated $8 billion in total revenue during fiscal 2024, which was a 16% increase from the year-ago period. That marked a deceleration from fiscal 2023, but there is a roaring trend beneath the surface.

Annual recurring revenue (ARR) attributable to Palo Alto's next-generation security (NGS) customers soared 43% to $4.2 billion in the fourth quarter. NGS refers to "platformization" customers. These are customers who have shifted the majority (or all) of their cybersecurity stack over to Palo Alto.

In the past, the cybersecurity industry was fragmented because many vendors only specialized in specific products, which meant businesses had to stitch their security stack together from multiple sources. That opened the door to unacceptable vulnerabilities, so providers like Palo Alto and CrowdStrike are now focused on "platforming" their customers.

Palo Alto says customers who use all three of its platforms have a lifetime value that is 40 times greater than customers who use just one. That presents a huge opportunity, so Palo Alto has offered many customers fee-free periods to help them transition away from their existing cybersecurity providers, which is a key reason why the company's total revenue growth has decelerated recently.

Over the long term, however, this strategy should pay off in a very big way.

Why Palo Alto stock is a long-term buy

Palo Alto thinks it can more than triple its NGS revenue to $15 billion by 2030, as it expects up to 3,500 of its top 5,000 customers to take a platform approach to cybersecurity by then. The majority of that revenue will be recurring, which builds predictability into Palo Alto's business for investors.

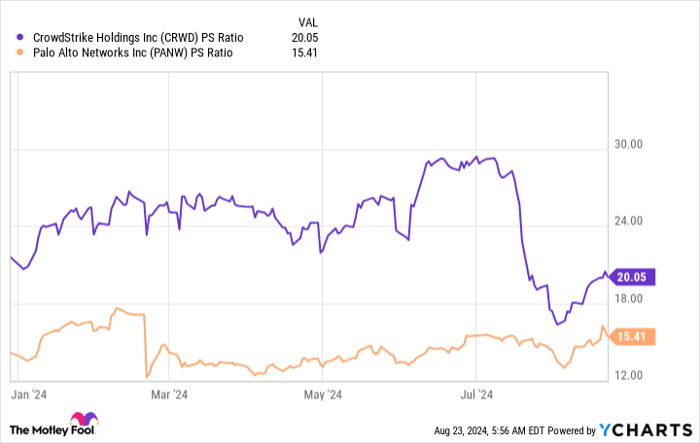

Palo Alto stock currently trades at a price-to-sales (P/S) ratio of 15.4, which makes it 23% cheaper than its main rival, CrowdStrike.

CrowdStrike consistently grows its total revenue more than 30%, so its stock might deserve a small premium under ordinary circumstances. But investors should consider two things:

Palo Alto's NGS revenue grew by 43% in the recent quarter, and its $4.2 billion in NGS ARR is more than CrowdStrike generates in total ARR.

CrowdStrike is coming off one of the most high-profile outages in history, which cost its customers an estimated $5.4 billion. The company has likely taken a big hit, but we won't know the magnitude until it reports its latest financial results on Wednesday, Aug. 28.

Therefore, I'd argue Palo Alto stock deserves to trade higher than where it is today. Its current valuation looks like a great entry point for investors, especially those who can stay the course for the next 10 years while the company reaps the rewards of platformization.

Should you invest $1,000 in Palo Alto Networks right now?

Before you buy stock in Palo Alto Networks, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palo Alto Networks wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 26, 2024

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike and Palo Alto Networks. The Motley Fool has a disclosure policy.