Should You Buy C3.ai Stock Right Now?

The hottest ticket in the technology industry right now, by far, is anything related to artificial intelligence (AI).

Much of the chatter surrounding AI has been reserved for megacap tech behemoths. However, smaller players have emerged as intriguing opportunities for growth investors too.

C3.ai (NYSE: AI) is an enterprise software platform specializing in AI-powered applications for both the public and private sectors. Yet despite the company's impressive growth, shares of C3.ai have declined 28% over the last year.

Is this an opportunity to buy a hidden gem in the AI space on sale, or are investors best off sitting on the sidelines?

Demand is high for C3.ai products, but ...

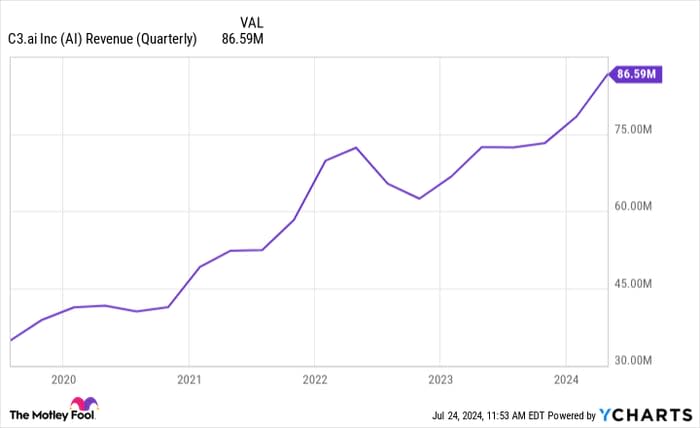

The chart below illustrates the revenue trend for C3.ai over the last five years. It's pretty clear the company has enjoyed steady momentum since AI became a focal point for the business world around the beginning of last year.

Data by YCharts.

One thing that I find particularly impressive about C3.ai is that despite its relatively small size, the company has managed to forge some impressive partnerships with cloud infrastructure platforms, including Microsoft, Alphabet, and Amazon, among others.

This partner network has proven to be a good source of lead generation, as evidenced by the company's rising deal flow. For the company's fiscal year 2024 (ended April 30), C3.ai closed 115 deals through its partner ecosystem, an increase of 62% year over year.

Another positive sign for C3.ai is how the company's generative AI products are sold across a multitude of end markets. Nearly 40% of its deals are in manufacturing and defense, but the remainder are sold across industries like life sciences, chemicals, energy, agriculture, and government contracting.

The company's expanding target market has likely contributed to its revenue acceleration. However, a closer analysis of its income statement sheds some light on where C3.ai is having issues.

Image source: Getty Images.

... the company's financial profile is upside down

The AI landscape is jam-packed with competitors of all sizes. And developing AI-powered software is both an arduous and expensive ambition.

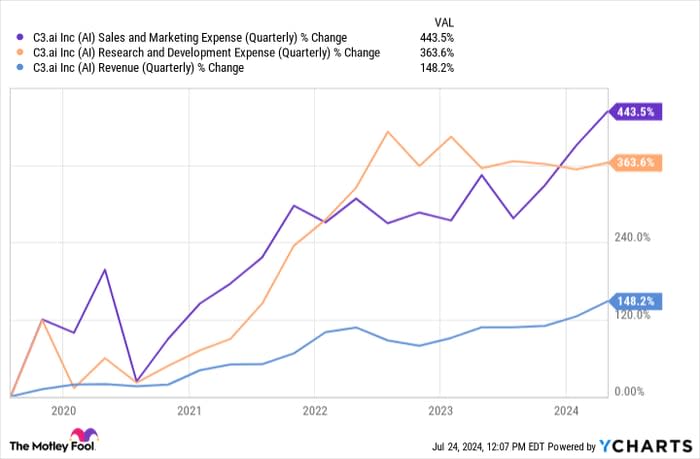

Data by YCharts.

As you can see above, the company's spending on sales and marketing as well as its investments in research and development have meaningfully outpaced revenue.

In fiscal 2024, C3.ai reported a net loss of $280 million and an adjusted operating loss of $95 million. Furthermore, the company's guidance for fiscal 2025 calls for additional adjusted operating losses of $125 million to $95 million.

These financial dynamics are unsustainable in the long run and could very well lead to a liquidity crunch at some point.

Is C3.ai a good stock to buy right now?

Performing a valuation analysis on C3.ai is a bit tough. Since the company is not yet profitable, the popular price-to-earnings (P/E) multiple isn't particularly useful. Moreover, some of the company's competitors such as Databricks are still private, making an accurate comparable company analysis nearly impossible.

Data by YCharts.

In the chart above, C3.ai is benchmarked against two other software-as-a-service (SaaS) AI players: Palantir and Snowflake.

With a price-to-sales (P/S) ratio of 10.5, C3.ai is actually the least expensive stock in this trio. While this might give the impression that C3.ai is cheap, there's good reason for its discounted valuation.

Palantir has witnessed a high degree of valuation expansion this year, but the company is consistently generating positive net income and free cash flow, not to mention its impressive growth among the private and public sectors. It's not surprising to see the company fetch a premium over its competition.

Conversely, Snowflake has witnessed a significant contraction in its valuation due to ongoing management changes and investor skepticism over the company's AI prospects.

Investing patterns in C3.ai seem to be somewhere in between Palantir and Snowflake. The company's valuation has indeed contracted but not as dramatically as Snowflake's.

However, it seems to me that investors see Palantir as a superior option overall when it comes to smaller enterprise software AI opportunities.

With all that in mind, investing in C3.ai makes little sense at the moment. The company is still undergoing a high degree of cash burn, and its growth -- while impressive -- is not enough to instill widespread conviction among investors that the company can take on its peers (or much bigger rivals).

There are better opportunities out there for AI growth investors, and C3.ai is best left out of your portfolio for now.

Should you invest $1,000 in C3.ai right now?

Before you buy stock in C3.ai, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and C3.ai wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Microsoft, and Palantir Technologies. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, Palantir Technologies, and Snowflake. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.