TSMC Profit Soars. Is Now a Great Time to Buy the Stock?

Shares of Taiwan Semiconductor Manufacturing (NYSE: TSM), or TSMC for short, didn't accelerate higher Thursday despite the semiconductor contract manufacturer reporting strong second-quarter results and lifting its guidance. Reports of tougher export restrictions on semiconductors coming from the U.S. government and comments from presidential candidate Donald Trump weighed on the stock.

Let's take a closer look at TSMC's most recent results and whether now is a good time to buy the stock following its recent sell-off.

Strong growth and improved outlook

For its second quarter, TSMC saw its revenue soar nearly 33% year over year to $20.8 billion, while its earnings per American depositary receipt (ADR) came in at $1.48, up from $1.14 a year ago. High-performance computing, which includes chips for artificial intelligence (AI), represented 52% of its revenue in the quarter and was up 28% quarter over quarter. Smartphone revenue accounted for a third of its sales and declined by 1% sequentially.

Customers continued to migrate to smaller nodes, with 5-nanometer processing technology accounting for 35% of its revenue, while 7nm processing technology was 17% and 3nm 15%.

The company projected third-quarter revenue to come in between $22.4 billion to $23.2 billion, representing 32% year-over-year growth and 9.5% growth sequentially. For the full year, it increased its guidance to growth slightly above the mid-20% mark compared to a prior outlook of low- to mid-20% revenue growth. TSMC also raised the low end of its full-year capital expenditure budget for the year, now expecting to spend between $30 billion and $32 billion, as it looks to increase capacity to meet demand. This capex spending should help power growth in future years.

Given its ongoing investment, TSMC said that both pricing and cost will play an important role in getting proper value for its investments and that its pricing will be strategic. The company added that it is currently in talks with its customers about its new 2nm technology and that it expects to ramp up more quickly than its 3nm technology did. It also noted that it does not expect the market to reach a balance for its AI accelerator and CoWoS advanced packaging capacity until sometime in 2025 or 2026.

Overall, this was a very strong quarter for TSMC, as revenue and profits soared and the company raised its full-year revenue guidance. However, the stock nonetheless was unable to get a lift as political commentary in the U.S. continued to weigh on the stock.

Image source: Getty Images.

Is now a golden opportunity to buy the stock?

When asked on its earnings call about Trump's comments about Taiwan needing to pay for its military and that it has taken 100% of the chip business from the U.S., TSMC management indicated it had no plans to change its strategy as it continues to build new capacity in various geographies including Arizona, Japan, and Europe. Given Taiwan's crucial role in the global semiconductor industry, though, in the event of any attack, it would appear to be in the best interests of the U.S. and its allies to protect the island to avert a catastrophe in the important semiconductor sector.

As for the potential of tighter Chinese restrictions, advanced chips are already restricted and China represents only about 16% of its revenue. I think the AI chip wave potential outweighs the risk in this area.

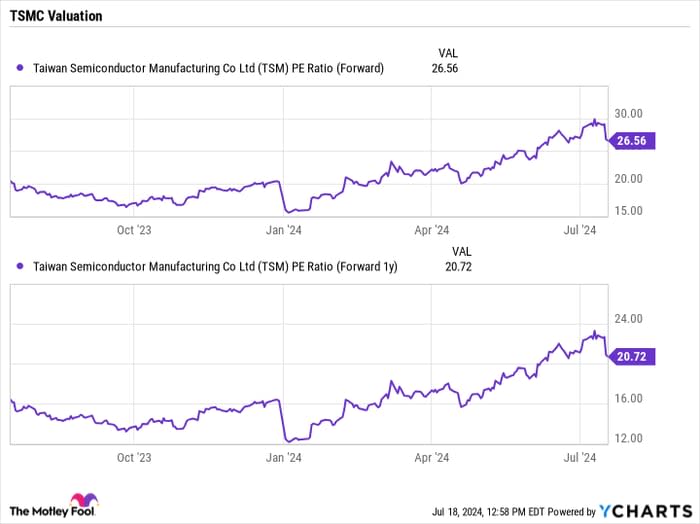

After the sell-off, meanwhile, TSMC's stock now trades at about a forward price-to-earnings (P/E) ratio of 26.6 times based on 2024 analyst estimates and under 21 times based on 2025 estimates.

TSM PE Ratio (Forward) data by YCharts

Given the opportunity in front of the company as the largest contract semiconductor manufacturer with key clients such as Apple and Nvidia, TSMC looks poised to ride the wave of increasing chip demand for AI applications, as well as any hardware upgrade cycle that may accompany the AI wave. Meanwhile, as more companies look to push into the AI chip space and TSMC shrinks node sizes, the company looks set to see solid pricing given the value it is giving to its customers.

As such, I would be a buyer of the stock on this recent dip. The company is performing well, its outlook is bright, and the geopolitical fears look overblown.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $741,989!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 15, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.