Nvidia Stock Correction: 25 Years of History Offers Its Take on How Far the Leading Artificial Intelligence (AI) Company Might Plummet

Although stock-split euphoria has taken hold in 2024, there isn't a bigger trend on Wall Street than the rise of artificial intelligence (AI).

The loose definition of AI involves the use of software and systems in place of humans for specified tasks. What gives this technology such broad-reaching potential spanning virtually every sector and industry of the global economy is the ability for AI-driven software and systems to learn without human intervention. Becoming more proficient at existing tasks over time, perhaps even learning new skills, gives AI the potential to add an estimated $15.7 trillion to the global economy by 2030, according to analysts at PwC.

No company has benefited more directly from this game-changing innovation than semiconductor colossus Nvidia (NASDAQ: NVDA).

Image source: Getty Images.

Nvidia has scaled at a truly phenomenal pace

Since 2023 began, Nvidia's stock has gained more than $2.4 trillion in market value, or 668% on a percentage basis, as of the closing bell on July 25, 2024. Nvidia also completed a 10-for-1 stock split in June to make its shares more nominally affordable for everyday investors.

This historic scaling of Nvidia's valuation has everything to do with its graphics processing units (GPUs) being the preferred choice by businesses operating AI-driven data centers. Though estimates vary, the analysts at TechInsights pegged Nvidia as being responsible for all but 90,000 of the 3.85 million GPUs shipped for use in data centers last year.

To build on this point, Wall Street's AI darling isn't anywhere close to meeting enterprise demand for its chips. When demand for a good or service handily outweighs its supply, it's normal for the price of said good or service to rise. Nvidia's phenomenal pricing power helped lift its adjusted gross margin by close to 14 percentage points over a period of five quarters (ended April 28).

There's also a lot of excitement surrounding Nvidia's next-generation data center hardware. The company's Blackwell platform, which accelerates computing in a half-dozen key areas, including generative AI solutions, is expected to be rolled out to customers later this year. By 2026, the Rubin GPU architecture, slated to run on a brand-new processor ("Vera"), should hit the market. In other words, Nvidia's lineup suggests it can retain its competitive edge, at least in terms of compute capabilities.

Despite this textbook expansion for Nvidia, shares of the company have recently hit the skids.

Image source: Getty Images.

Nvidia is in correction territory: Here's how far history suggests it could fall

When the closing bell tolled on July 25, Nvidia's stock clocked in at $112.28 per share. While this is, as noted, a 668% gain from where it was on Jan. 1, 2023, shares are down 20.2% from the $140.76 all-time intra-day high reached on June 20. In other words, Nvidia's stock is in a full-blown correction.

Although there isn't a predictive tool or metric that can forecast where Nvidia's stock will find its bottom with 100% accuracy, 25 years' worth of history does offer clear clues of what might await this AI leader in the months and quarters to come.

Over the last quarter of a century, we've witnessed no shortage of buzzy technologies and trends come and go. While some of these innovations and trends have gone on to make investors considerably richer over the long run, one of the key consistencies of next-big-thing innovations is the early-stage overestimation of their adoption and utility by the investing community.

While it's easy to be swept away by grandiose addressable market figures (e.g., AI adding $15.7 trillion to the global economy by 2030), it's important to recognize that all new technologies and trends need time to mature. Though there's no way to know ahead of time how long it'll take for an innovation to mature, the simple fact that most businesses lack a clear game plan with their AI investments suggests we're witnessing the next in a long line of bubbles.

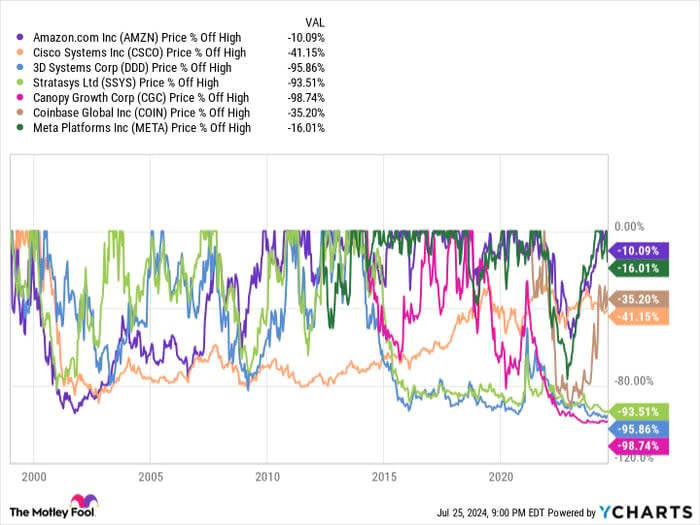

More specifically, 25 years of next-big-thing innovations have shown that market leaders within these trends tend to be hit the hardest:

When the dot-com bubble burst, leading e-commerce player Amazon and networking giant Cisco Systems each lost in the neighborhood of 90% of their value on a peak-to-trough basis.

Although genome decoding stocks like Celera and Human Genome Sciences are no longer around -- they were both acquired many years back -- both companies followed in Amazon's and Cisco's footsteps and shed most of their value after the euphoria surrounding genome decoding faded.

Whereas e-commerce and networking have been long-term winning investments, the excitement surrounding 3D printing has evaporated. Following their peak, both 3D Systems and Stratasys lost well over 90% of their respective value.

Though cannabis isn't a new technology, its legalization in Canada was viewed as a generational moneymaking opportunity. Unfortunately, Canadian licensed producer Canopy Growth eventually plunged 99% from its peak valuation.

Cryptocurrency exchange Coinbase Global has served as the stock-based face of the crypto revolution. When the buzz surrounding crypto and blockchain technology ebbed, shares of the company plummeted by close to 90%.

Meta Platforms spearheaded the rise of the metaverse -- the virtual 3D environment where people can interact with each other and create an entirely new ecosystem. However, with this technology needing time to mature, Meta's stock ultimately fell by around 80% before rebounding to new highs.

Based on what we've witnessed from next-big-thing innovations and trends over the last 25 years, market leaders tend to shed 80% or more of their peak market value once the bubble bursts.

The good news for Nvidia is that it had multiple well-established sales channels before artificial intelligence became its primary growth driver. These channels include its GPUs used for gaming and cryptocurrency mining, as well as its professional visualization and automotive/robotics solutions. If the AI bubble were to burst, just like every other next-big-thing trend over the prior 30 years, Nvidia would likely find more downside support than many of the pummeled market leaders that came before it.

Nevertheless, there's a precedent that market-leading stocks plummet once the realization sets in that a buzzy technology needs time to mature. At the very least, history points to Nvidia losing a minimum of half its value on a peak-to-trough basis. This would bring its share price down to $70 and imply significant downside.

But if Nvidia isn't the exception to the rule, history suggests it could plummet below a $1 trillion market cap in the years to come.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Sean Williams has positions in Amazon and Meta Platforms. The Motley Fool has positions in and recommends Amazon, Cisco Systems, Coinbase Global, Meta Platforms, and Nvidia. The Motley Fool recommends 3d Systems. The Motley Fool has a disclosure policy.