Is It Too Late to Buy CrowdStrike Stock?

There's little doubt that cloud-based cybersecurity standout CrowdStrike (NASDAQ: CRWD) is the hot security stock on Wall Street this year. Shares are up a whopping 145% over the past 12 months. The stock's success is no coincidence; the company continues to grow quickly and profitably quarter after quarter.

But sometimes, share prices run so hard that they get ahead of the underlying business. Is that the case with CrowdStrike?

If you're looking at CrowdStrike's long-term future, there's a lot to be excited about. The question is whether shares are still trading at an attractive valuation today. Here is what you need to know.

CrowdStrike is built for long-term growth

Constant product innovation and expansion have been CrowdStrike's secret recipe for remarkable growth and investment returns. CrowdStrike is a cloud-based cybersecurity software company that began in endpoint security but has expanded into various other types over time. Adding products has considerably expanded its addressable market from $19 billion to $100 billion today.

The company sells its technology a la carte as product modules, meaning customers can pick and choose what they want to pay for. However, the company's product quality is steadily attracting more customer dollars. Today, approximately 28% of CrowdStrike's customers pay for at least seven modules, and those who pay for eight or more nearly doubled year over year in the first quarter of its fiscal year 2025 (its most recently reported quarter). In other words, companies are consolidating their cybersecurity needs on CrowdStrike's platform, which has helped drive strong revenue growth for an extended time.

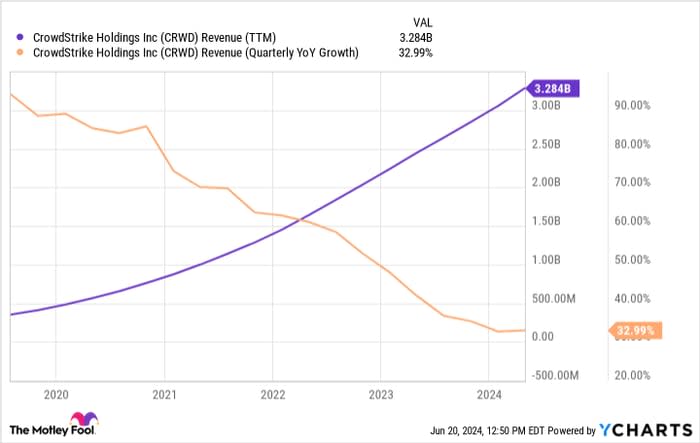

CrowdStrike is still growing at an impressive 33% clip despite now doing over $3.2 billion in annual revenue:

CRWD Revenue (TTM) data by YCharts

The resilient growth is an argument for how mission-critical CrowdStrike's products are to its customers. The average enterprise breach can cause over $4 million in damages, so companies looking to slash spending will probably not cut their cybersecurity budgets if they can help it.

Zooming out shows a crystal-clear opportunity. CrowdStrike's management estimates that its $100 billion addressable market could grow to $225 billion by 2028. Remember that CrowdStrike's $3.2 billion revenue is a low single-digit percentage of today's market opportunity. CrowdStrike could grow for years as it takes market share and the overall "pie" grows larger over time.

Where does CrowdStrike's valuation stand today?

The stock market is forward-looking. A company can have all the room to grow in the world, but knowing how much of that potential the market has already priced into the stock is essential. CrowdStrike has become a massive company for a business doing $3.2 billion in sales; the stock's market cap is roughly $95 billion. That's a price-to-sales ratio of approximately 30, which is very high compared to almost any company on Wall Street today.

It's a similar story if you look at earnings. CrowdStrike's forward P/E is 95. Yes, CrowdStrike's profits will rapidly grow moving forward. Analysts call for an average of 22% growth over the next three to five years. Unfortunately, CrowdStrike will need to significantly outperform those expectations to justify the scorching hot valuation it commands today.

Whether you look at the top or bottom line, CrowdStrike has seemingly gotten quite far ahead of its business fundamentals. The market is pricing sky-high growth expectations into shares, and investors could be poised for an eventual letdown.

What should investors do?

There's little argument that CrowdStrike is a fantastic business and deserves its flowers. The product receives numerous accolades across the industry, and the growth and margins show that CrowdStrike's product is in hot demand and that customers are willing to pay for it.

But a great business doesn't always work out as an investment. The valuation is often so out of whack that it stunts investment returns. A stock can wait years for business fundamentals to catch up to the share price.

CrowdStrike looks like it's in a similar situation, so investors should stay on the sidelines until shares trade at a more attractive valuation. This stock needs to cool off before it makes sense again.

Should you invest $1,000 in CrowdStrike right now?

Before you buy stock in CrowdStrike, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CrowdStrike wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $775,568!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike. The Motley Fool has a disclosure policy.