Warren Buffett's Berkshire Hathaway Just Sold Snowflake Stock. You'll Never Believe Which Beaten-Down Value Stock It Bought Instead

On Aug. 14, Warren Buffett's conglomerate Berkshire Hathaway (NYSE: BRK.A)(NYSE: BRK.B) released its updated stock holdings for the second quarter of 2024. The biggest headline-grabbing moves were that it sold all of its shares of Snowflake (NYSE: SNOW) and started a roughly $260 million position in Ulta Beauty (NASDAQ: ULTA). But both of these moves make perfect sense for Berkshire.

To be clear, Berkshire Hathaway has plenty of money -- it had $277 billion as of its latest report. In short, it can buy virtually anything it wants; it didn't have to sell one stock to buy another. But allow me to explain how Buffett thinks about investing and why it consequently makes perfect sense for him to swap out Snowflake for Ulta Beauty in Berkshire's portfolio now.

Here's why (I think) Snowflake stock is out

Berkshire Hathaway invested in Snowflake stock during its 2020 initial public offering (IPO), which may be the only time it bought an IPO stock. However, one of Buffett's proteges Todd Combs was a Snowflake customer at Geico and was conversing with Snowflake's former CEO Frank Slootman.

This checks two important boxes for Buffett's investing style: A personal relationship with leadership and familiarity with the product. Throughout the years, Buffett sought to buy companies and retain the leadership he trusted. And Buffett is often quoted as saying, "Never invest in a business you cannot understand."

This likely wasn't true for Buffett personally with Snowflake stock. But Combs likely did know Slootman, and he was familiar with the business as a customer.

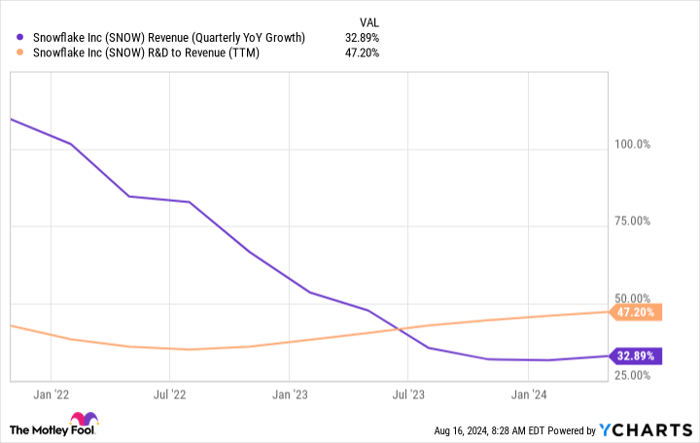

However, things may be changing for Snowflake, and this likely contributed to Berkshire selling in the second quarter. The company reports financial results for its fiscal 2025 Q2 on Aug. 21. But as of Q1, management only expected 24% growth in fiscal 2025, down sharply from 38% growth in 2024. Moreover, its expenses are increasing as it invests more in artificial intelligence (AI).

The chart below shows that research and development expenses are rising as a percentage of revenue, reflecting its investment in AI. But this isn't necessarily paying off with better growth.

SNOW Revenue (Quarterly YoY Growth) data by YCharts.

At Berkshire's annual meeting in 2018, Buffett said, "We still love a business that takes very little capital and earns high returns, and continues to grow, and requires very little incremental capital." By contrast, Snowflake is spending to keep up with competition when it comes to AI, which isn't what Buffett prefers.

Not only that, Snowflake named Sridhar Ramaswamy as its CEO earlier this year. He may be up for the task, but Combs had a personal connection with Slootman. So this may have played into Berkshire's decision to sell Snowflake stock as well.

Here's why (I think) Ulta Beauty stock is in

Ulta Beauty operates about 1,400 brick-and-mortar retail stores selling cosmetic products and offering beauty services. Like Snowflake, growth has slowed -- Ulta Beauty only expects about 3% top-line growth this year. But the difference is it doesn't have to spend heavily to stay out in front of trends because the space doesn't change much. This leaves ample cash for rewarding shareholders.

Consider that even in this upcoming slow year, Ulta Beauty expects to have a 14% operating margin -- that's really strong for a retail business. It expects to open about 60 new locations this year while remodeling about 40 more, which does have some cost. But it's modest compared to its profits. Moreover, it doesn't have any debt, meaning creditors don't have any claim on its future profits.

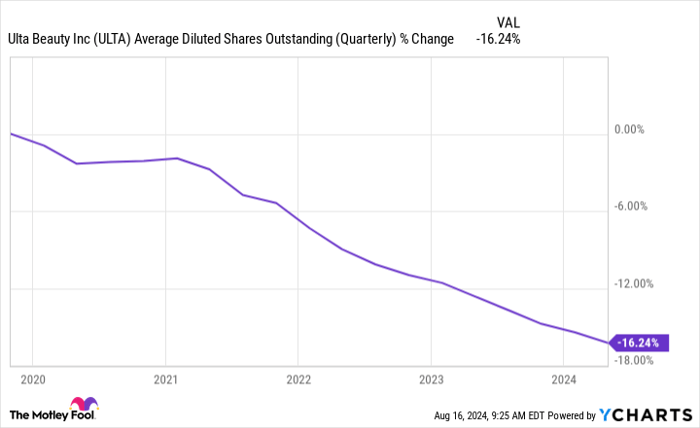

This situation leaves most of Ulta Beauty's profits for shareholders. Management intends to use $1 billion to repurchase shares in 2024 alone. For perspective, its market cap is only $17 billion as of this writing. And in fact, the company has diligently repurchased shares for years, as the chart below shows.

ULTA Average Diluted Shares Outstanding (Quarterly) data by YCharts.

With Ulta Beauty, Buffett likely sees a simple business that's easy to understand, requires little incremental capital to stay competitive, and earns a strong profit while returning capital to shareholders. This simple scenario can make Ulta Beauty stock a winner over the long haul.

As the icing on the cake, Ulta Beauty stock has dropped about 35% from its highs and is now trading at one of its cheapest valuations ever at just 14 times its earnings. That's cheap -- and cheaper than most other comparable businesses. This bargain valuation makes it even more likely that the stock will earn positive returns from here, making it an ideal candidate for Berkshire Hathaway's portfolio.

Should you invest $1,000 in Ulta Beauty right now?

Before you buy stock in Ulta Beauty, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ulta Beauty wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $779,735!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway, Snowflake, and Ulta Beauty. The Motley Fool has a disclosure policy.