Why Snowflake Stock Dropped 12% Last Month

Shares of data storage and analytics company Snowflake (NYSE: SNOW) dropped by 12.4% during August, according to data provided by S&P Global Market Intelligence. The stock got crushed after the company reported results for its fiscal 2025 second quarter on Aug. 21 -- but the drop in price confused many investors.

Here's why the stock's drop was confusing for some: In the quarter, Snowflake generated product revenue of $829 million, which was way ahead of the $810 million that had been the top of management's guidance range. Moreover, management subsequently raised its full-year revenue guidance. In other words, business seems to be better than expected.

However, the profit trends look problematic. The company expects its adjusted gross profit margin to drop from 78% in fiscal 2024 to 75% in its fiscal 2025, and its adjusted operating margin is expected to fall from 8% to 3%.

True, Snowflake's revenue trends are better than expected and management increased its top-line guidance. But its guidance for its profit metrics didn't improve, which was another reason for concern.

Where's Snowflake's money going?

Snowflake is a data company, and the artificial intelligence (AI) trend is fueled by data, which would seem to indicate that this should be Snowflake's moment to shine. But building out the infrastructure necessary to support AI comes at a cost. The company's expenses for research and development are quickly rising as it buys equipment and hires workers to build compelling AI products and features.

That trend is likely to continue for the company. It has a usage-based revenue model, so it generates more revenues as its customers use its platform more. And right now, enterprises are curious about AI, so that can expand platform usage. Therefore, investments in AI will continue, but they will be a drag on the bottom line for some time.

Is there any hope for Snowflake's shareholders?

The good news for Snowflake's shareholders is that many of its key business metrics -- customer counts, retention rates, etc. -- are still trending in the right direction. To share just one stat, the company now has more than 10,000 customers compared with around 8,500 a year ago. That's strong growth.

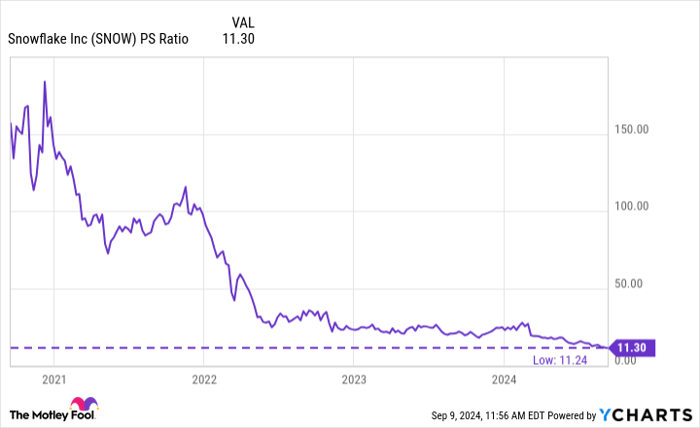

Moreover, trading at 11 times sales, Snowflake stock has never been cheaper, as the chart below shows.

SNOW PS Ratio data by YCharts.

Snowflake's business still has some strong points, and the stock's valuation has come way down. That's good. But unfortunately, even that lower valuation still assumes plenty of growth and profit expansion over the long term. Therefore, the company does need to find ways to grow and eventually exercise some operating leverage. Shareholders will need to be patient for now, recognizing that some of those improvements may still be far away.

Should you invest $1,000 in Snowflake right now?

Before you buy stock in Snowflake, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Snowflake wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $630,099!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 9, 2024

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Snowflake. The Motley Fool has a disclosure policy.